Is a senior citizen having dividend income and capital gain income required to pay advanced tax?

Income Tax is collected from taxpayers in various forms such as TDS, Advance Tax, and Self-Assessment Tax as applicable. As per Section 2(1) of the Income Tax Act 1961, "advance tax" means the advance tax payable in accordance with the provisions of Chapter XVII-C.

As per section 208 every person whose estimated tax liability for the year exceeds Rs. 10,000, shall pay his tax in advance in the form of “advance tax”.

Thus, any taxpayer whose estimated tax liability for the year exceeds Rs. 10,000 has to pay his tax in advance by the due dates prescribed in this regard.

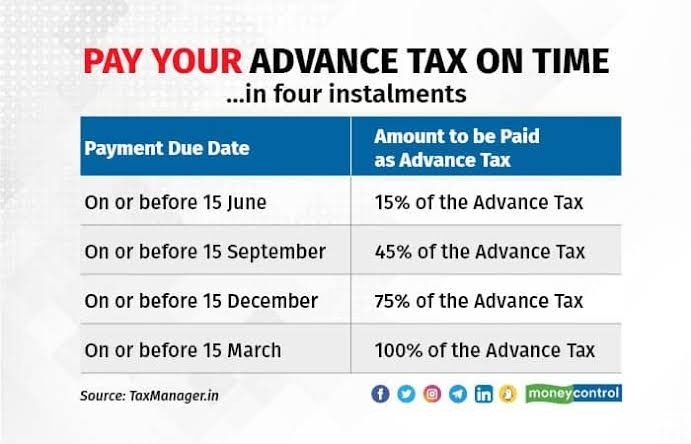

Due date for payment of advance tax are as follows:

Advance tax is to be paid in different instalments. The due dates for payment of different instalments of advance tax are as follows:

However, any person opting for the presumptive taxation scheme under section 44ADA/44AD is liable to pay whole amount of advance tax on or before 15th March of the previous year.

Exemption from Payment of Advance Tax:

As per section 207, a resident senior citizen (i.e., an individual of the age of 60 years or above) not having any income from business or profession is not liable to pay advance tax.

In other words, if a person satisfies the following conditions, he will not be liable to pay advance tax:

1) He is an individual

2) He is resident in India as per the Income-tax Act

3) He is of the age of 60 years or above at any time during the year

4) He is not having any income chargeable to tax under the head “Profits and gains of business or profession”

What are the consequences on failure to pay advance tax?

A) Consequences of Interest and Late fees

If you fail to pay Advance Tax or pay at a rate less than stipulated rates you will be required to pay Interest under sections 234B & 234C of the Income Tax Act, 1961.

Interest under sections 234B –

Interest @1% per month on shortfall amount is payable if 90% of the tax is not paid before the end of the Financial year. This is for "Default in payment of Advance tax".".

Interest under section 234C-

Interest @1% per month on shortfall amount is payable if the tax is not paid as per the instalments schedule. This is for "Deferment in Instalments of Advance tax"

B) Consequences of Order or Notice from Assessing Officer

If taxpayer fails to pay advance tax (or advance tax paid is lower than the required amount) and he has already been assessed by way of regular assessment in respect of the total income of any previous year, then the Assessing Officer may pass an order under section 210(3) requiring him to pay advance tax on his current year’s income (specifying the amount of instalments in which tax should be paid). Such an order may be passed during the financial year, but not later than the last day of February.

On receipt of the notice from the Assessing Officer to pay advance tax, if the taxpayer’s estimate is lower than the estimate of the Assessing Officer, then the taxpayer can submit his own estimate of current income/advance tax and pay tax accordingly. In such a case, he has to send intimation in Form No. 28A to the Assessing Officer.

Alternatively, if the advance tax on current income as per own estimate of the taxpayer is likely to be higher than the amount estimated by the Assessing Officer, the taxpayer shall pay such higher amount as advance tax in accordance with his own calculation. In such a case, no intimation to the Assessing Officer is required.

The Assessing Officer can revise his order issued to the taxpayer to pay advance tax (as discussed above) under section 210(4). Such revision can be done, if subsequent to the passing of an order to pay advance tax but before 1st March of the relevant financial year a return of income in respect of any later year has been furnished by the taxpayer or any assessment for any later year has been completed at a higher figure. On receipt of such order, the procedure to be followed by the taxpayer will be same as discussed earlier.

Conclusion:

Therefore, a resident senior citizen is not required to pay any advance tax if he/she does not have any income taxable under the head “Profits and gains from business or profession even though he has income from Income from Other Sources or Income from Capital Gains.

A resident senior citizen, defined as an individual of the age of 60 years or above. It is important to note that the exemption from payment of advance tax is available only to resident senior citizens. Non-resident senior citizens, who are not residents of India as per the Income-tax Act, are not eligible for this exemption.

In case a senior citizen has income chargeable to tax under the head "Profits and gains of business or profession," they would be required to pay advance tax as per the prescribed due dates. Failing to pay advance tax may attract interest and penalty under the Income Tax Act 1961.

Talk to our team.

A 30-minute call with our team — no deck, no follow-up email blasts. Just a read on how this applies to your facts.